Your ally in efficient

& intelligent trading.

Discover a new standard of futures and forex trading, where cutting-edge platforms and genuine support work hand in hand to elevate your success.

“To suggest that you are in good hands with GFF would be a gross understatement.”

Drew M.

Futures Trader — 9+ yrs

25+

Platforms

4.9★

Trustpilot

100+

Countries Served

$50

Min Margin

Trusted Platforms

Everything we do starts with one goal — helping traders execute with confidence, transparency, and the right tools at their fingertips.

25+ Platforms

Low Commissions

Phone Support

Industry-leading margins on micro e-mini futures

Start trading with as little as $250. Our competitive day trading margins let you maximize your capital efficiency across the most popular micro e-mini contracts.

View All MarginsMicro E-minis Futures

Day Trading Margin**Day Trading Margins & Minimum account size valid for select FCMs only. Margins are subject to change.

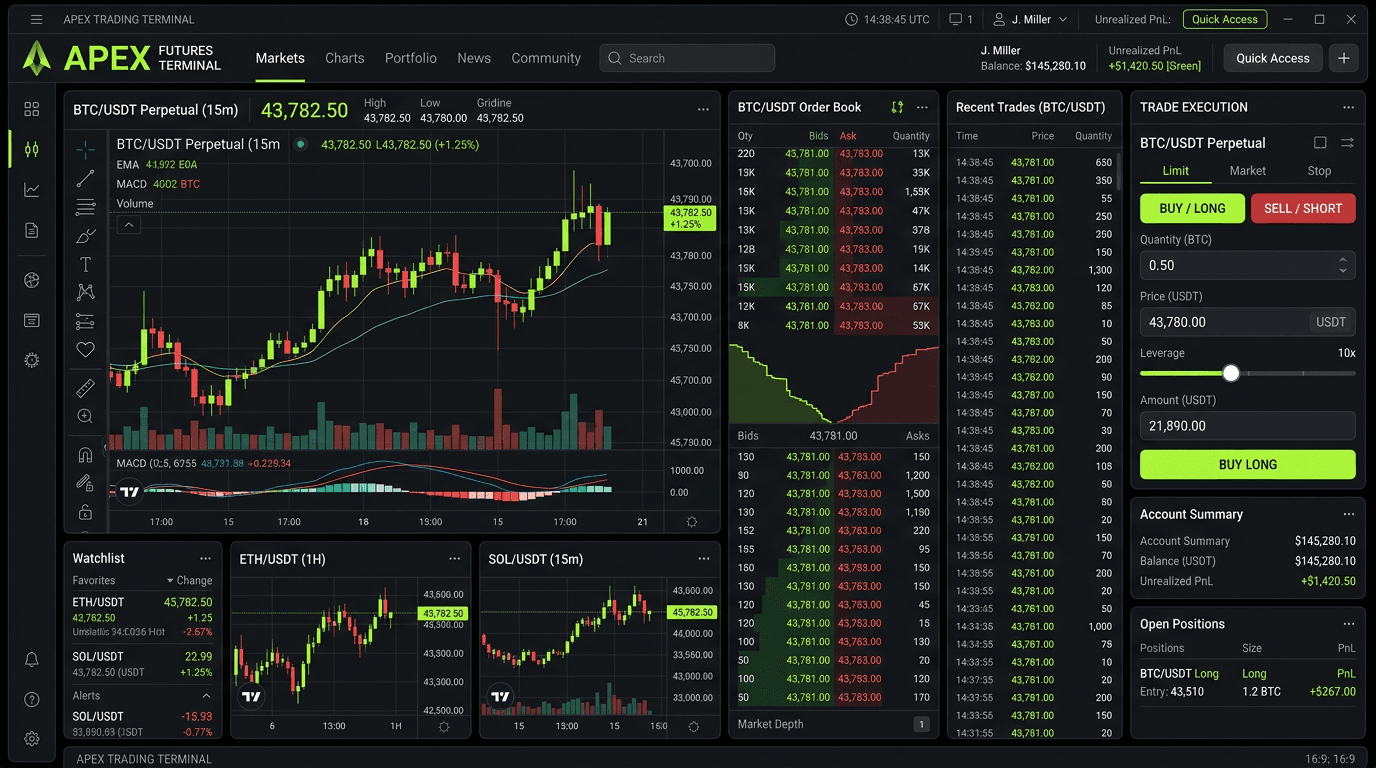

A modular platform designed to scale

Trader Growth

Yearly25+ Trading Platforms

From TradingView to Sierra Chart — choose the platform that matches your trading style.

Competitive Margins

Access some of the lowest intraday margins in the industry across multiple FCM clearing firms.

Leader-Follower Program

Mirror trades from experienced professionals automatically.

Real-Time Analytics

Harness real-time market data to refine strategies and sharpen execution.

Fast Execution

Go live with lightning-fast order execution and reliable connectivity.

Dedicated Support

Get help when you need it with a support team that genuinely cares about your success.

Multiple Platforms

Choose from 25+ platforms — professional desktop terminals, web-based solutions, and mobile apps.

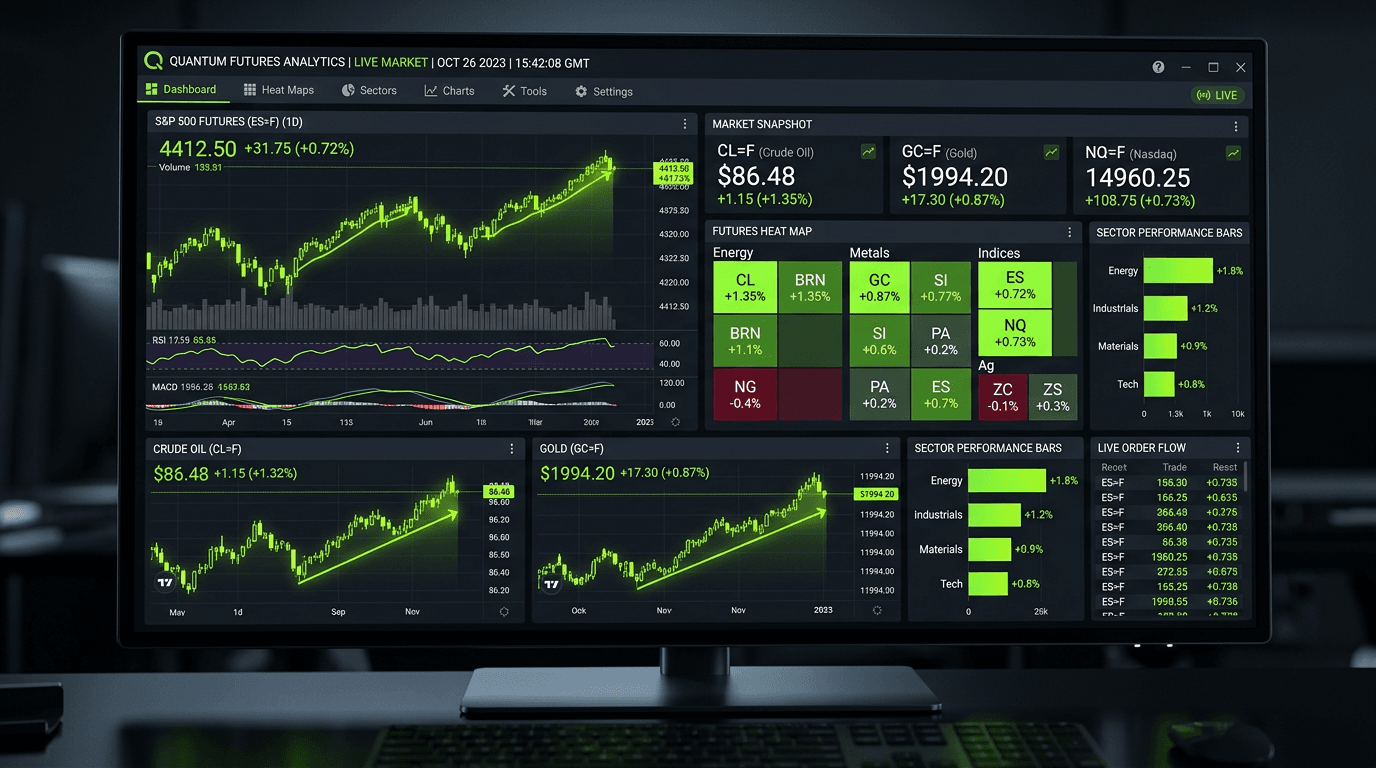

Market Analytics

Real-time data feeds, advanced charting, and analytics tools to sharpen your edge.

Expert Workspace

A complete trading environment designed for serious futures and forex traders.

NFA Member & CFTC Registered

Verified Broker

Make your trading impossible to limit

Level up your trading with GFF Brokers — a next-generation brokerage built for clarity, precision, and market excellence.

“Great customer service! Ready, available , friendly and fast with solutions.....”

John B.

Trader

FAQ

Common questions

GFF Brokers provides access to futures, options on futures, and forex markets. You can trade popular products like E-mini S&P 500, Micro E-minis, crude oil, gold, currencies, and many more across global exchanges.

You can open an account with as little as $250. Day trading margins on micro e-mini products start from just $50 per contract, making futures trading accessible to traders of all levels.

The Leader-Follower program allows you to automatically mirror the trades of experienced professionals who trade with their own capital on the line. You select the leaders you want to follow, set your risk parameters, and trades are executed automatically in your account.

We support 25+ trading platforms including NinjaTrader, TradingView, Sierra Chart, Rithmic R|Trader, Bookmap, MultiCharts, and many more. Each platform offers unique features to match different trading styles and strategies.

We provide dedicated customer support via phone, email, and live chat. Our team consists of knowledgeable trading professionals who can assist with platform setup, account questions, and technical issues. We pride ourselves on fast response times and genuine care for our clients.

Subscribe to Our Newsletter

Stay updated with the latest market news, trading insights, and GFF Brokers announcements.